What to do with your 401k when you change jobs?

Move your money into an Individual Retirement Account (IRA) This choice gives you maximum control and flexibility. With a 401 (k) plan, the employer chooses the investments and makes the rules—and the rules vary from plan to plan. With an IRA, you’re in charge. Unlimited investment choices instead of a small menu.

Do you roll your 401k into a new account?

Some fees are really low in 401 (k) plans, so you may want to roll your old 401 (k) into your new one. Having everything in one account, instead of having multiple 401 (k) plans from different jobs, helps keep your retirement savings streamlined, Berra said.

What happens to my 401k If I leave my job?

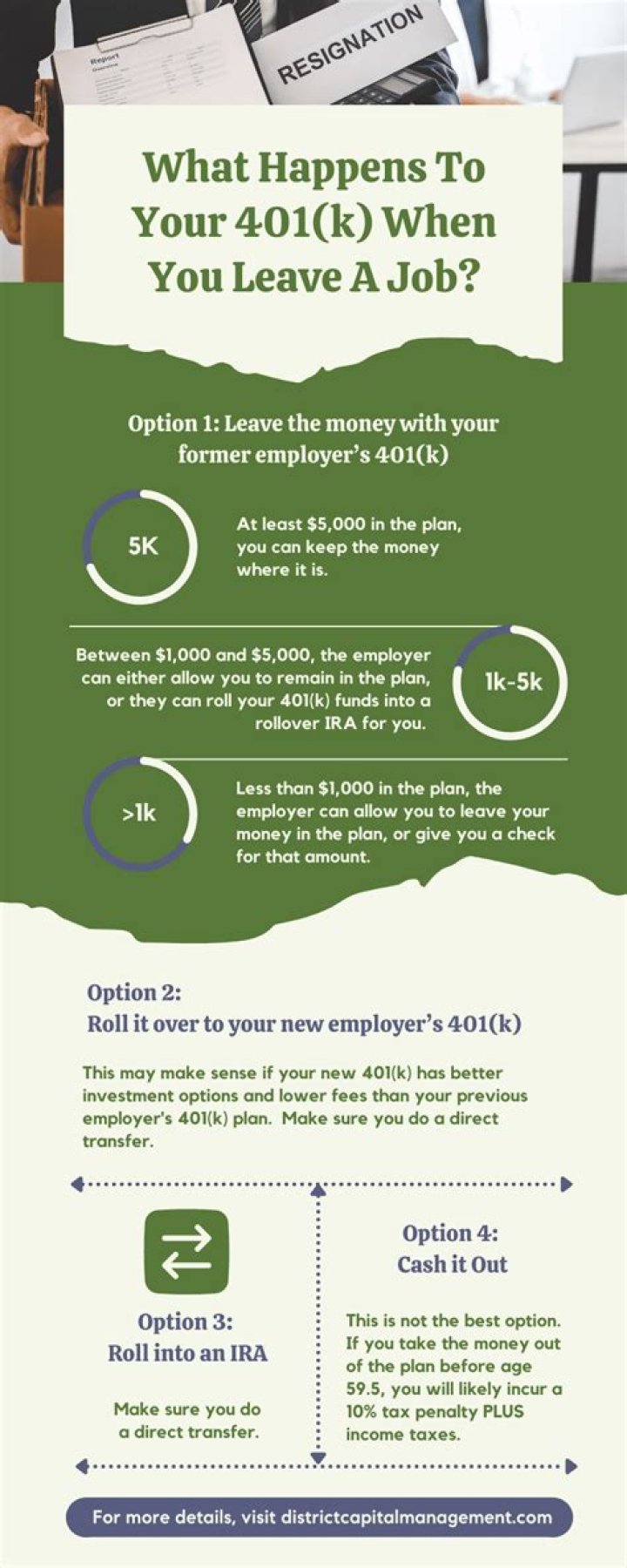

Here are the available alternatives. If you opt to leave your 401 (k) where it is, your contributions will cease — as will any match your employer made — but your investments will stand and, hopefully, continue to grow. Many employers require at least a $5,000 balance to do this.

How long can I keep money in my former employer’s 401k?

Keep your money in your former employer’s 401 (k) plan This is your legal right if you have at least $5,000 in your account. Ask how long you have to decide. In most cases, you get 30 to 90 days.

What should I do with my 401k rollover?

Whether you pick an IRA for your rollover or choose to go with your new employer’s plan, consider a direct rollover—that’s when one financial institution sends a check directly to the other financial institution. The check would be made out to the bank or brokerage firm with instructions to roll the money into your IRA or 401 (k).

How long do you have to move your 401k After leaving a job?

How Long Do You Have to Move Your 401 (k) After Leaving a Job? You have 60 days to roll over a 401 (k) into an IRA after leaving a job–but there are many other options available to you in these circumstances when it comes to managing your retirement savings.

Can a former employer cash out your 401k?

Keep your money in your former employer’s 401 (k) plan This is your legal right if you have at least $5,000 in your account. Ask how long you have to decide. In most cases, you get 30 to 90 days. If your account holds under $5,000, your employer has the option of cashing you out of the plan.

Are there limits on how much you can contribute to a 401k when you change jobs?

While most plans have measures in place to prevent employees from exceeding these limits, it is not uncommon for excess contributions to occur, particularly when employees change jobs during the year and participate in more than one employer’s plan.

How often do you change your 401k plan?

According to the Bureau of Labor Statistics, the average US worker changes jobs 12 times throughout a career. If you leave a 401 (k) plan behind at each job and, come retirement, you will have to sort through a trail of plans to figure out what you have.

What happens to your 401k when you leave a job?

If you leave a 401 (k) plan behind at each job and, come retirement, you will have to sort through a trail of plans to figure out what you have. Additionally, you risk overpaying for too many unnecessary investments. To be sure, if you have been through a layoff and are not sure of your next move,…

Do you have to roll over your 401k to a new plan?

Almost all 401 (k) plans now accept rollovers from other retirement plans. You should certainly contribute to your new plan. But should you transfer your old account into it? Consolidating your retirement money makes it easier to manage.

What happens to my 401k If I leave my job at 55?

Also, if you left your job during or after the calendar year in which you turned 55, you won’t owe an early-withdrawal penalty. You’ll owe income taxes on your money. If you’re in a 30% combined federal and state tax bracket, for example, and cash out a $50,000 account, you’ll have only $35,000 left after taxes.

How are 401k withdrawals work when you’re unemployed?

There’s another option for getting your hands on distributions without being charged the 10% penalty. Unemployed individuals can receive what is termed substantially equal periodic payments (SEPP) from 401(k) plans under the IRS’ 72(t) rule.